2026-01-24

(Code snippets for this post can be found in the Github repository.) Update: added discussion and a new fitting algorithm

In the previous post, we extended the Smooth Transition Exponential Smoothing (STES) model from Taylor (2004) and Liu et al. (2020) by replacing the linear model in STES with a XGBoost model.

We saw that the XGBoost model has lower MAE and MedAE scores, but generally underperform STES in terms of RMSE. We did not however find out the true cause of this. In this post, we drill down into the cause of this, and propose a different fitting algorithm.

Recall that the XGBSTES model is formulated as

\begin{equation} \begin{aligned} \sigma_t^2 &= \alpha_{t-1} r_{t-1}^2 + (1-\alpha_{t-1})\widehat{\sigma}_{t-1}^2 \\ \alpha_{t-1} &= \mathrm{sigmoid}\left(\mathcal{F}(X_{t-1})\right) \\ \end{aligned} \end{equation}

We fit the model by minimizing mean squared error (MSE) between the forecasted variance \sigma_t^2 and realized squared returns.

\mathtt{loss} = \frac{1}{T}\sum_{t=1}^{T}\left(r_t^2 - \widehat{\sigma}_t^2\right)^2

For each time step t, the forecasted variance \sigma_t^2 is a weighted combination of the previous period’s squared return r_{t-1}^2 and the previous forecast \widehat{\sigma}_{t-1}^2. The weight \alpha_{t-1} is produced by an XGBoost model applied to the transition variable X_{t-1} and passed through a sigmoid so it lies in (0,1). In other words, we do not predict next-day variance directly; instead, we predict a time-varying update weight and then generate the variance forecast recursively over contiguous blocks of the feature matrix.

XGBoostXGBoost is a general-purpose engine for functional gradient descent. At its core, it optimizes an objective function by iteratively adding base learners f_j(x) to an ensemble. The model at step j is F_j(x) = \sum_{k=1}^j f_k(x). Each base learner can be either a regression tree (gbtree) or a linear model (gblinear).

XGBoost does not optimize the loss directly. Instead, at each step j, it approximates the loss using a second-order Taylor expansion around the current prediction z_i^{(j-1)}. If we wish to minimize a loss \mathcal{L} = \sum_i \ell(y_i, z_i), XGBoost solves for the term f_j(x_i) that minimizes:

\mathcal{L}^{(j)} \approx \sum_{i=1}^N \left[ \ell(y_i, z_i^{(j-1)}) + g_i f_j(x_i) + \frac{1}{2}h_i f_j^2(x_i) \right] + \Omega(f_j)

where g_i = \partial \ell / \partial z_i is the gradient and h_i = \partial^2 \ell / \partial z_i^2 is the Hessian. The term \Omega(f_j) penalizes the complexity of f_j. We minimize this loss function with respect to f_j, and the term \ell(y_i, z_i^{(j-1)}) depends only on the previous rounds and is a constant that can be dropped from this step.

This formulation means that to adapt XGBoost to any problem, we only need to provide two arrays: the gradient vector g and the Hessian vector h. How the library uses these arrays to update the ensemble depends on which base learner we choose. We describe both options below; for XGBSTES we use the linear booster (gblinear).

gbtree)We include the tree derivation for completeness. It illustrates how XGBoost uses g and h to build each round and motivates the regularization mechanics that reappear in the scaling discussion later.

In gbtree mode, the function f_j is a regression tree. A regression tree maps a data point x_i to a leaf node m and assigns it a score w_m. i.e.

f_j(x_i) = w_{m(x_i)}

where m(x_i) is if-else rule that maps x_i to the leaf node m, w is the vector of scores for all leaves. The \mathcal{L}^{(j)} above sums over all x_i, and we can rewrite it as a summation over all M leaf groups. Let I_m = \left[i \mid m(x_i) = m\right], \mathcal{L}^{(j)} and the regularization term

\Omega(f_j) = \gamma M + \frac{1}{2}\lambda\sum_{m=1}^M w_m^2

can be written as

\mathcal{L}^{(j)} \approx \sum_{m=1}^M \left[ \left(\sum_{i \in I_m} g_i\right) w_m + \frac{1}{2} \left(\sum_{i \in I_m} h_i\right) w_m^2 \right] + \gamma M + \frac{1}{2}\lambda\sum_{m=1}^M w_m^2

We minimize this loss function with respect to f_j, or rather, the weight vector w. The constant term \ell(y_i, z_i^{(j-1)}) does not depend on w, so it can be removed in the optimization. Rewrite G_m = \sum_{i \in I_m} g_i and H_m = \sum_{i \in I_m} h_i. We can rearrange the terms to get

\mathcal{L}^{(j)} \approx \sum_{m=1}^M \left[ G_m w_m + \frac{1}{2} \left(H_m + \lambda \right) w_m^2 \right] + \gamma M

This is a sum of quadratic equation in w_m and its minimum is achieved at

w_m^* = -\frac{G_m}{H_m + \lambda}

Note that \gamma M is also a constant at this step and drops out of the optimization. The \gamma M term only plays a role when XGBoost decides the split. Once we plug in w_m^* back into L and simplify, we get

\mathrm{Score} = -\frac{1}{2} \sum_{m=1}^M \frac{G_m^2}{H_m + \lambda} + \gamma M

XGBoost then calculates the “Gain” of a split, it drops the negative sign (to convert Loss to Gain) and compares Score(Left) + Score(Right) - Score(Parent). XGBoost creates a split if the Gain is above a certain threshold, and \gamma acts to reduce the gain from each split

The library handles the tree construction, finding splits that maximize the reduction in this regularized quadratic loss. The interaction between the magnitude of our derivatives (G, H) and the regularization parameters (\lambda, \gamma) becomes critical when we discuss the scaling problem later.

gblinear)In gblinear mode, the ensemble collapses to a single linear model:

F(x) = w^\top x + b

Rather than building trees, XGBoost updates the weight vector w directly using coordinate descent. At each boosting round, for each feature j, the library computes the aggregate gradient and curvature along that feature:

G_j = \sum_{i=1}^N g_i \, x_{ij}, \quad H_j = \sum_{i=1}^N h_i \, x_{ij}^2

and updates the weight:

w_j \leftarrow w_j - \eta \frac{G_j + \lambda w_j}{H_j + \lambda}

where \eta is the learning rate. The regularization term is an elastic net penalty:

\Omega(w) = \frac{1}{2}\lambda \|w\|_2^2 + \alpha_{\mathrm{reg}} \|w\|_1

controlled by reg_lambda (\lambda) and reg_alpha (\alpha_{\mathrm{reg}}). Tree-specific hyperparameters (max_depth, min_child_weight, gamma) do not apply to gblinear; the relevant controls are reg_lambda, reg_alpha, and learning_rate.

Note that the coordinate descent update has the same G/(H + \lambda) structure as the optimal leaf weight in gbtree. The regularization mechanics are analogous: when \lambda dominates the denominator, the gradient signal is suppressed.

gblinear for XGBSTESIn XGBSTES, the gate \alpha_t = \text{sigmoid}(\mathcal{F}(X_t)) maps a scalar model output through a sigmoid. A linear model \mathcal{F}(X_t) = w^\top X_t + b is a natural choice here: each feature’s contribution to the gate is directly readable from its weight, and coordinate descent converges faster than tree construction. We use the configuration booster="gblinear", updater="coord_descent", reg_lambda=1.0 for all XGBSTES results in this post and subsequent posts in the series.

Why is the Hessian a vector in

XGBoostFor a dataset of size N, the Hessian is strictly an N \times N matrix. However,

XGBoost(and most boosting libraries) requests a vector of size N. This is becauseXGBoostcannot handle an N \times N matrix due to memory constraints. For 1 million rows, the matrix has 10^{12} entries and is in general not feasible to store. Computationally, inverting or decomposing this matrix to find optimal tree splits is also impossible (O(N^3)).To make the problem solvable,

XGBoostmakes a diagonal approximation. It assumes that for the purpose of finding the next split, the rows are independent. It ignores the cross-dependencies and only asks for the diagonal elements:h_i = \frac{\partial^2 L}{\partial z_i^2}

and the “Hessian” becomes a N-dimensional vector. This independence assumption is why the method is an approximation. However, because we update the model iteratively (boosting), errors from this approximation are corrected in subsequent rounds, allowing

XGBoostto converge even with this simplified curvature information.

Writing v_t \equiv \widehat{\sigma}_t^2 for brevity, we chose to break the dependency loop to avoid computing the recursive gradient and Hessian vectors. If we assume the variance path is fixed, we can algebraically invert the recursion to find the “optimal” gate \alpha_t^* that would minimize the error at a single step. Rearranging the recursion equation for \alpha_t:

\alpha_t^* = \frac{r_{t+1}^2 - v_t}{r_t^2 - v_t}

We can then train XGBoost to predict this target \alpha_t^* from features X_t, using a standard squared error objective. This transforms the recursive problem into a standard supervised regression problem.

This method aligns with Expectation-Maximization (EM) algorithms often used in latent variable models. We treat the unobservable gate \alpha_t as a latent variable. In the ‘E-step’, we infer the optimal gate values given the data; in the ‘M-step’, we train the model to predict these values. This transforms a difficult sequential optimization problem into a simpler supervised regression task—effectively generating an intermediate “Teacher” (the algebraic inversion) to guide the learner.

However, in our specific context, this Teacher is numerically brittle. The denominator in the equation above is the difference between the squared return and the current variance estimate. When the market is quiet or when the forecast is accurate, this denominator approaches zero, causing the target \alpha_t^* to explode or flip signs arbitrarily. The model effectively learns from an unstable “Oracle” that provides high-variance instructions and optimizes a noisy surrogate rather than the true recursive error.

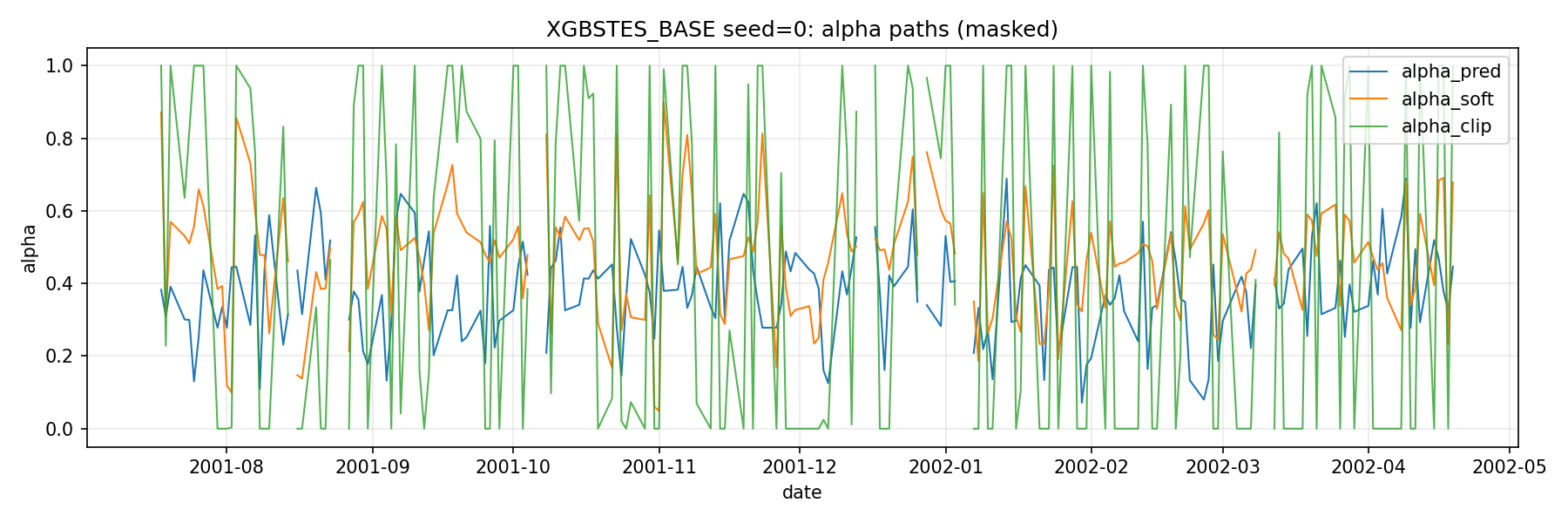

Indeed this brittleness is the cause of our model underperforming STES. The “Teacher” of our model is an ill-tempered one. Figure 1 below shows the \alpha_t^* (alpha_clip) vs the prediction from the tree model (alpha_pred).

The realized variance are extremely noisy, pushing the implied \alpha^* to either 0 or 1 after clipping most of the time, and is undefined when v_t = r_t^2. The real variance process obviously do not follow the simple recursive relationship. As a result, our model learns an \alpha process that is roughly around 0.4. The constant ES fit has \alpha_{ES} = 0.101.

The theoretically correct approach is to compute the exact gradient of the cumulative loss L = \sum \ell_t with respect to the model outputs z_t, accounting for the full recursive chain by backpropagating through time.

We define the adjoint variable \delta_t as the sensitivity of the total loss to the variance state v_t:

\delta_t = \frac{\partial L}{\partial v_t} = \frac{\partial \ell_t}{\partial v_t} + \frac{\partial v_{t+1}}{\partial v_t} \delta_{t+1}

From the STES recursion, the term \frac{\partial v_{t+1}}{\partial v_t} = (1 - \alpha_t). Substituting this into the equation, we get a backward recurrence relation:

\delta_t = (v_t - r_t^2) + \delta_{t+1}(1 - \alpha_t)

This recursion mirrors the forward pass but runs backward in time. Once we have computed the adjoints \delta for the entire sequence, we can compute the correct gradient g_t for the XGBoost input z_t:

g_t = \frac{\partial L}{\partial z_t} = \delta_{t+1} \frac{\partial v_{t+1}}{\partial \alpha_t} \frac{\partial \alpha_t}{\partial z_t} = \delta_{t+1} (r_t^2 - v_t) \alpha_t (1 - \alpha_t)

For the Hessian h_t, calculating the exact second derivative involves complex terms including the second derivative of the recursion itself. Instead, we employ the Gauss-Newton approximation. We treat the model as locally linear and approximate the Hessian using the square of the Jacobian of the model output with respect to the parameters. This simplifies to:

h_t \approx \left( \frac{\partial v_{t+1}}{\partial z_t} \right)^2 = \left[ (r_t^2 - v_t) \alpha_t (1 - \alpha_t) \right]^2

In our recursive model like STES, the off-diagonal terms (e.g., \frac{\partial^2 L}{\partial z_1 \partial z_5}) are not zero. Changing the gate at t=1 changes the variance at t=5. The true Hessian is a dense, lower-triangular matrix. However, this approximation is numerically stable and guarantees a positive Hessian, which is essential for the convexity required by XGBoost.

Gauss-Newton approximation is a standard technique in non-linear least squares optimization. We approximate the curvature of the loss function by assuming the underlying model is locally linear, effectively ignoring the second-order complexity of the model itself.

Our objective function L(z) is a composition of two functions: 1. The Prediction Model f(z): Maps the input margin z to a prediction \hat{y} (in our case, the variance v). 2. The Loss Function \ell(\hat{y}, y): Measures the error. For Least Squares, this is \ell = \frac{1}{2}(\hat{y} - y)^2.

L(z) = \frac{1}{2}(f(z) - y)^2

To find the gradient, we apply the Chain Rule:

L'(z) = (f(z) - y) \cdot f'(z)

and to find the Hessian, we differentiate L'(z) again. Product Rule yields:

L''(z) = \underbrace{(f'(z))^2}_{\text{Term 1}} + \underbrace{(f(z) - y) \cdot f''(z)}_{\text{Term 2}}

- Term 1: The square of the Jacobian. This term is always positive.

- Term 2: The interaction between the current error and the second derivative of the model f(z).

The Gauss-Newton method drops Term 2.

h_{GN} \approx (f'(z))^2

We justify this simplification for three reasons: 1. Small Residuals: If the model is fitting well, the term (f(z) - y) is small (close to zero), making Term 2 negligible. 2. Linearization: We assume that locally, the model f(z) is linear, implying f''(z) \approx 0. 3. Convexity: Term 1 is a square, so it is guaranteed to be non-negative (h \ge 0). Term 2 involves f''(z), which can be negative. If the total Hessian becomes negative, XGBoost sees a “concave” objective (like a hill instead of a valley) and the optimization diverges. The approximation forces the objective to be convex.

When we initially ran the End-to-End method, we found that the model refused to learn. The linear model would not update its weights, effectively outputting a constant prediction. The root cause lay in the interaction between the scale of our data and the regularization mechanics of XGBoost.

Financial returns are small numbers; a daily return of 1% is 0.01, and a squared return is 10^{-4}. Consequently, the prediction errors (r_{t+1}^2 - v_{t+1}) are of order 10^{-4}, and the sensitivities (r_t^2 - v_t) are also of order 10^{-4}. The gradient g_t, being the product of these terms, falls to the order of 10^{-8}.

Recall the gblinear coordinate descent update:

w_j \leftarrow w_j - \eta \frac{G_j + \lambda w_j}{H_j + \lambda}

where G_j \approx 10^{-8} and H_j \approx 10^{-8} (the Gauss-Newton Hessian squares the Jacobian, which is of the same order as the sensitivity), and the default regularization parameter \lambda = 1, the denominator is dominated by \lambda. The gradient term G_j is negligible relative to \lambda, so the update reduces to \Delta w_j \approx -\eta w_j — the model only shrinks existing weights toward zero and the gradient signal vanishes entirely. The same issue arises in gbtree mode: the structure score G^2/(H + \lambda) falls to \approx 10^{-16}, and splits are never accepted.

This is analogous to the scaling issues found in Lasso or Ridge regression, where unstandardized features can lead to disproportionate penalization. Here, the “feature” is the gradient signal itself. To fix this, we multiply returns by 100 before squaring them. This scales the variance targets by 10,000. The gradient, which is quadratic in the scale of returns, increases by a factor of 10^8, bringing it to order O(1). With this adjustment, the standard XGBoost hyperparameters function as intended.

Note: The

min_child_weightparameter discussed below applies only to thegbtreebooster. Thegblinearbooster used inXGBSTESdoes not usemin_child_weight; its regularization is controlled entirely byreg_lambdaandreg_alpha.The

min_child_weightrelates to the Hessian and measures the quantity of the curvature or the number of samples in a leaf. A split is only allowed if H_L \ge \text{min\_child\_weight} and H_R \ge \text{min\_child\_weight}. In second order optimization, the curvature measures the steepness of the surface. When curvature is high, a small change in prediction changes the error massively. The model has a strong motivation to split here. On the other hand, when the curvature is small, the loss function is a flat plain. The optimizaer can change the prediction wildly and the error barely changes. The model would have no strong incentive to split here.To see how the quantity of curvature relates to the number of sample, we only need to look at the mean squared error objective function.

\ell = \frac{1}{2} \left(\hat{y} - y\right)^2 \rightarrow \frac{\partial^2 \ell}{\partial \hat{y}^2} = 1

H_m = \sum_{i\in I_m} 1

is just the number of sample.

The Hessian in logistic regression varies depending on how confident the model is. The Hessian for a single data point i is:

h_i = p_i (1 - p_i)

where p_i is the predicted probability. If the model predicts p = 0.5, then h_i = 0.5 \times 0.5 = 0.25 is at the maximum curvature. The loss function is steep and a split here make sense. If the model predicts p = 0.99, then h_i = 0.99 \times 0.01 \approx 0.01. The model is already sure about this prediction. The loss function is flat and the model should decide not to split further.

min_child_weightmeasures whether there is there enough unsolved data?

Even after we apply the scale adjustment, the XGBoost algorithm has many other tunable hyperparameters. Moreover, validating a recursive model requires care. Standard K-fold cross-validation breaks the temporal structure, and standard time-series splits fail to account for the hidden state v_t. If we start a validation fold at time T, we cannot simply initialize v_T with the global starting variance; we must “warm start” the filter to reflect the accumulated history.

We implemented a custom Time-Series Cross-Validation loop that approximates the initial state for each validation fold using the realized variance of the recent training data (v0_va below).

def run_cv_e2e(self, X, y, returns, ...):

# ...

for fold_idx, (train_idx, valid_idx) in enumerate(tscv.split(X_np)):

# Slice data for this fold

X_tr, X_va = X_np[train_idx], X_np[valid_idx]

r2_tr, r2_va = returns2_np[train_idx], returns2_np[valid_idx]

# Warm Start Initialization for Validation

# We approximate v_start using the mean of the last 20 days of training data

v0_va = float(np.mean(r2_tr[-20:]))

# Create custom objectives bound to this fold's data

feval = self._make_e2e_objective(

returns2=r2_va, y=y_va, init_var=v0_va

)[1]

# Train and Evaluate

# ...This ensures that our cross-validation scores accurately reflect the model’s ability to maintain a volatility forecast over time, rather than measuring its ability to recover from a bad initialization.

We evaluated both the Alternating (Algorithm 1) and End-to-End (Algorithm 2) implementations on SPY returns from 2000 to 2023. Both XGBSTES variants use the gblinear booster with coordinate descent (updater="coord_descent", reg_lambda=1.0). We also added the cross-validation to Algorithm 1 for comparison so the number might be different from the last post.

| Model | IS RMSE | OS RMSE |

|---|---|---|

| ES | 5.06e-4 | 4.64e-4 |

| STES-EAESE | 4.98e-4 | 4.49e-4 |

| XGBSTES-EAESE (Algorithm 1) | 5.18e-4 | 4.35e-4 |

| XGBSTES-EAESE (Algorithm 2) | 5.02e-4 | 4.43e-4 |

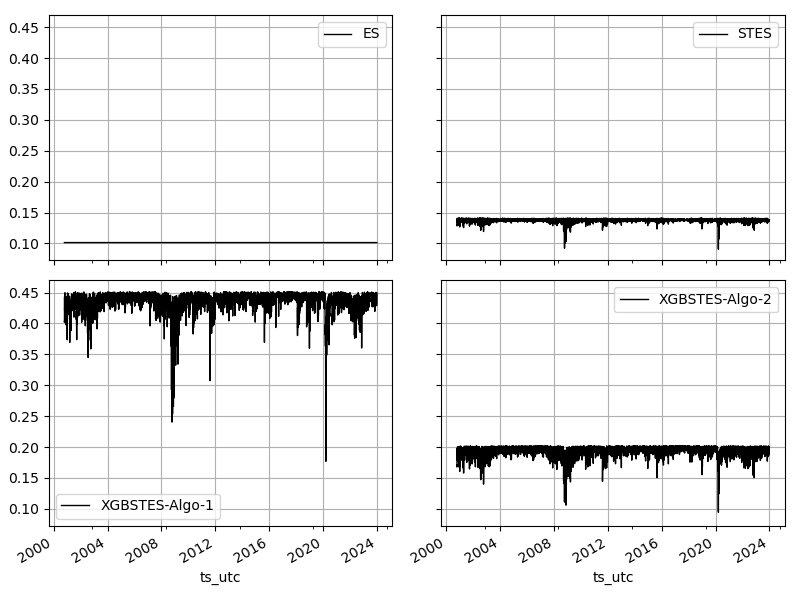

Even though the Algorithm 1 has the lowest OS RMSE, its in-sample performance is inferior to all other algorithms. A more informative comparison would be on the alpha values. Figure 2 below shows that XGBSTES-EAESE (Algorithm 1) still suffers from learning the brittle \alpha^* target. XGBSTES-EAESE (Algorithm 2), on the other hand, produce more sensible \alpha values.

That’s it for this post. We will diagnose the XGBSTES model further in future posts. See you then.